By InvestaX | April 2026

Maritime finance has always operated on large numbers and long timelines. A single commercial vessel can cost tens of millions of dollars. Financing one typically requires specialist lenders, technical assessments, and months of documentation. For shipowners with strong assets and clear revenue streams, the process still works. But it is slow, concentrated, and often inaccessible to operators below a certain size.

Tokenization offers a complementary pathway. It does not replace bank debt, nor remove the structural complexity of maritime finance. But it opens an additional channel that can move faster, reach a broader investor base, and operate within a regulated framework that institutions already understand.

This article explains how tokenized ship financing works in practice, what the deal structure looks like, what issuers need to consider before pursuing this route, and why Singapore has emerged as a natural base for this type of activity.

What Tokenized Ship Financing Actually Involves

At its core, tokenized ship financing converts a financial interest in a maritime asset into a digitally issued security, typically structured as debt or equity and distributed through a regulated platform.

The mechanics are relatively straightforward. A vessel, or a fleet of vessels, is held within a legal entity, usually a Special Purpose Vehicle (SPV). That SPV issues tokens representing either:

- A loan to the shipowner (debt), or

- An ownership stake in the vessel (equity)

Investors subscribe to these tokens through a licensed tokenization platform like InvestaX. Returns – whether interest payments on a loan or a share of charter revenue – flow back to token holders.

What changes with tokenization is the distribution infrastructure, not the underlying economics. The vessel still generates revenue the same way. The borrower still has repayment obligations. The legal protections still rest on conventional financial and maritime law. What differs is how the financing is packaged, who can access it, and how efficiently capital can be raised across jurisdictions – a key driver behind the growth of maritime finance tokenization.

The Capital Gap Tokenization Is Addressing

To understand why tokenized ship financing is gaining traction, it is important to look at where traditional maritime finance becomes less efficient.

The global shipping finance market was valued at approximately $167 billion in 2024, according to market research firm Grow Market Reports, and is projected to grow to around $284 billion by 2033. Large shipping companies with strong balance sheets continue to access capital through syndicated loans, export credit agencies, and capital markets. The gap emerges in the mid-market.

These are operators with real assets and operating revenue, but without the scale or banking relationships required by major shipping lenders. For this segment, access to capital is often constrained not by asset quality, but by timing and structure.

This dynamic is particularly visible across maritime economies in Asia.

A useful illustration comes from the recent webinar, “Unlocking Indonesia’s Maritime Market with Pegasus 2,” moderated by InvestaX Co-founder Alice Chen. Speakers including Iko Johansyah (Chairman of the Indonesia Maritime University Alumni association), Young Kim (CEO of Galactica), and Pilsup Shim (CEO of PT Pelayaran Maritim Prima) highlighted how financing constraints continue to shape fleet development in Indonesia.

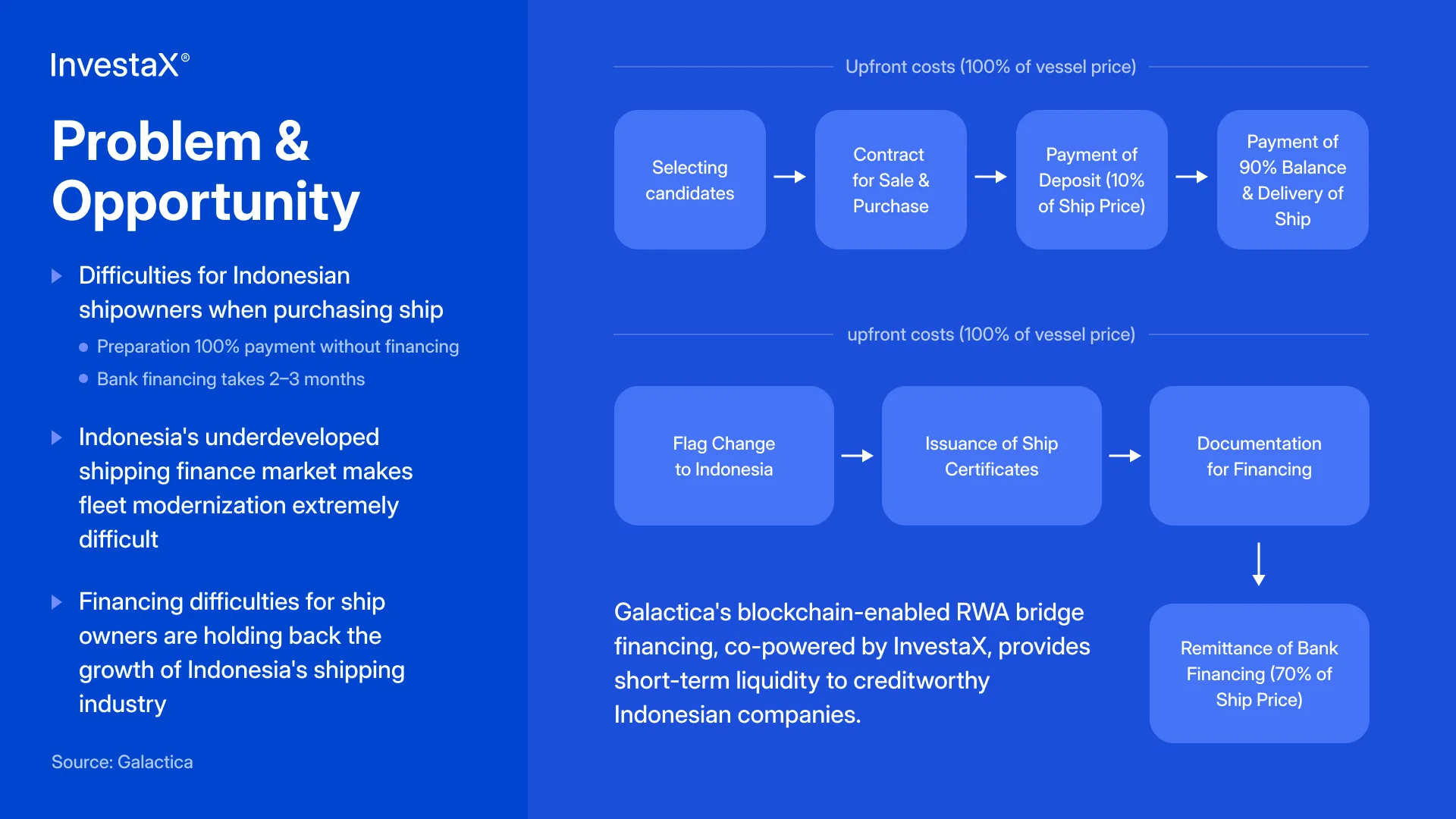

As discussed during the session, vessel financing in markets such as Indonesia typically follows a sequential process. Shipowners are often required to acquire the vessel upfront, paying close to 100% of the purchase price. The vessel is then registered and appraised, after which bank financing is arranged – a process that can take between two to six months. Even then, financing may cover only 70-80% of the vessel’s appraised value.

The result is a clear funding gap at a critical point in the transaction. Operators who have secured both the asset and charter contracts are required to bridge this period with significant capital already deployed.

This is where bridge funding solutions, including tokenized structures, become relevant.

Indonesia provides a strong structural example. As the world’s largest archipelagic nation, with more than 17,000 islands, around 90% of domestic logistics moves by sea. The country is also a major exporter of commodities such as coal, nickel, and copper, all of which depend on maritime transport.

At the same time, fleet modernization remains an ongoing challenge. A significant portion of the commercial fleet is aging, while mid-tier operators continue to face difficulty accessing conventional bank financing on competitive terms.

The result is a disconnect between capital demand and supply – one that maritime asset tokenization is increasingly positioned to address.

To watch the recording of the webinar “Unlocking Indonesia’s Maritime Market with Pegasus 2,” please contact us.

The Pegasus transaction: a reference point from execution

In January 2026, Galactica launched Pegasus 1, a tokenized ship financing product designed to provide funding and financing for bridges, addressing the liquidity gap between vessel acquisition and bank disbursement.

Galactica is a Singapore-based RWA issuer focused on maritime asset tokenization, particularly Indonesian shipping assets. It works with established operators such as PT Pelayaran Korindo, a maritime group with over five decades of operating history, to originate and structure deals.

In January 2026, Galactica completed the closing of Pegasus 1, a $25 million LNG vessel financing. The transaction was issued and distributed through InvestaX, operating under its Capital Markets Services and Recognised Market Operator licences from the Monetary Authority of Singapore. Settlement was conducted on-chain via Kaia's blockchain infrastructure.

The deal structure was straightforward: a bridge loan against a 145,000 CBM LNG vessel supporting fleet modernisation in Indonesia. The vessel was acquired and operational. The shipowner had initiated bank financing, which was in process. Galactica provided the short-term capital – the bridge – while the bank financing completed. Once the bank disbursed, the bridge loan was repaid, and investors received their principal and interest.

Galactica's second issuance, Pegasus 2, launched in March 2026, was structured more efficiently precisely because the first deal had already confirmed what worked.

The underlying asset was already revenue-generating at the time of issuance. Investors were not financing a plan – they were financing a vessel already operating under charter. This is a meaningful point for credit assessment: the asset profile was transparent and verifiable, not speculative.

Investor eligibility followed conventional securities law. The offering was made available to accredited and institutional investors through InvestaX's platform, with full KYC and AML processes applied at onboarding. The regulatory framework was that of a standard securities offering – digitally distributed, but compliant with the same obligations that govern traditional private placements.

Together, these elements reflect a broader principle: tokenization works best when the financial and legal architecture is already sound, and the technology simply extends its reach.

How issuers typically structure a maritime tokenization deal

The legal structure of a tokenized maritime deal generally follows one of two approaches, depending on whether the instrument is debt or equity.

Debt (loan-based) structure:

The shipowner or operator receives a loan from an SPV. The SPV issues tokens representing the loan – effectively debt instruments – to investors. Investors receive interest payments over the loan's tenure. On maturity or repayment, the principal is returned. This is the most common structure for shorter-term maritime financing, including bridge loans. It is familiar to institutional fixed-income investors and aligns well with standard credit assessment frameworks.

Examples of tokenized ship financing issued this structure are Pegasus 1 and Pegasus 2, both issued and distributed via InvestaX.

Equity structure:

The vessel or fleet is held by an SPV, and tokens represent fractional equity ownership. Token holders receive a share of the vessel's operating revenue – typically charter income – over time. This suits longer-term investments where the shipowner is looking for permanent or semi-permanent capital rather than short-term bridge financing.

The choice between these structures depends on the financing need, the shipowner's preference for capital structure, and the investor profile being targeted. Bridge financing and working capital facilities generally suit a debt structure. Fleet development or vessel acquisition with long charter contracts may be better suited to equity.

In both cases, a few structural elements are consistent:

- SPV wrapper: The vessel or the loan obligation sits inside a purpose-built legal entity, separate from the operating company. This gives investors a defined claim on specific assets and protects them from the broader liabilities of the shipowner's business. In some jurisdictions – Indonesia being one example – regulatory constraints on offshore SPV incorporation mean that the SPV is established domestically, under local licensing, rather than in a neutral offshore jurisdiction. This is a material consideration for legal structuring and requires jurisdiction-specific advice.

- Transfer restrictions: Tokens representing securities are subject to transfer restrictions under securities law. Investors must be verified and whitelisted before they can hold or receive tokens.

- Investor eligibility: Tokenized maritime securities are typically limited to accredited and institutional investors. Retail participation in most jurisdictions requires additional regulatory approvals that are not yet widely available for this asset class.

- Reporting obligations. Issuers are responsible for providing token holders with ongoing information about the asset's performance, such as charter contract status, revenue, material changes, and anything that might affect repayment or distributions.

What the capital structure looks like compared to traditional ship finance

For issuers evaluating tokenized ship financing against conventional bank debt, the practical differences are worth examining.

- Speed to close. Traditional ship finance transactions can take several months, driven by credit approvals, documentation, and lender coordination. Tokenized structures, particularly for bridge financing, can be arranged more quickly once the structure is defined and investors are onboarded. In transactions like Pegasus, tokenization was used specifically to bridge a multi-month financing gap, rather than replicate the full bank lending process.

- Investor pool. Traditional ship finance often relies on a relatively concentrated group of banks and maritime lenders. Tokenization expands access to a global pool of accredited investors, including family offices, private credit funds, and digital asset-native investors.

- Minimum ticket sizes. Direct participation in vessel financing often requires multi-million dollar commitments, particularly in bilateral or syndicated deals. Through vessel tokenization, these exposures can be divided into smaller units, like a $50,000 ticket, allowing participation at lower thresholds while still targeting qualified investors.

- Ongoing covenants. Bank financing typically comes with covenants: minimum liquidity ratios, restrictions on additional borrowing, requirements to maintain insurance. Tokenized instruments can include equivalent protections through smart contract conditions or legal documentation, but these need to be deliberately designed.

- Compliance infrastructure. Traditional financing moves compliance work to the lender's credit and legal teams. Tokenized financing moves it to the issuance platform's compliance infrastructure. The work does not disappear, it shifts. Issuers should expect to engage with KYC processes, investor eligibility certification, and regulatory disclosure obligations, in the same way they would for any securities offering.

Tokenization makes maritime finance accessible to a different set of investors, through a faster and more digitally native distribution channel, within a regulated framework. For issuers who need speed, broader reach, or access to capital that conventional banks are not positioned to provide, it is a meaningful additional option.

What issuers should consider before pursuing tokenized ship financing

Tokenization extends access to capital. But it does not change the fundamental criteria that determine whether a maritime financing deal is investable.

Before pursuing this route, issuers should assess the following:

- Asset profile: Operating vessels with verifiable charter contracts or stable revenue are typically the most straightforward candidates, as they provide clearer visibility on credit quality and repayment. However, earlier-stage or uncontracted assets can still be financed, depending on structure, sponsor strength, and risk appetite, though they generally require stronger justification to investors.

- Vessel type and liquidity: Different vessel types carry different risk profiles in a default scenario. Smaller, more widely traded vessel types – tugs and barges, coastal tankers, general cargo vessels – are typically easier to liquidate or redeploy exterior than specialized large-scale carriers. For shorter-tenure instruments, this matters: investors will want confidence that the underlying asset can be realised if repayment does not occur as planned.

- Deal size: The compliance, legal, and operational infrastructure required to issue a tokenized security carries fixed costs that do not scale down proportionally with deal size. Deals below a certain threshold, broadly, below $1 million, may find the cost-benefit case harder to make. The economics generally strengthen as deal size increases, and as the issuer builds the infrastructure for a repeatable programme rather than a one-off transaction.

- Repeatability: The most efficient tokenized maritime financing programmes are structured as ongoing programmes with a defined asset profile, rather than ad hoc single deals. Each transaction validates and refines the legal structure, the investor onboarding process, and the operational workflow. By the second or third deal in a programme, the marginal cost and complexity of each issuance decreases significantly.

- Investor relations capacity: Tokenized investors, like any securities holders, have ongoing information rights. Issuers should be prepared to provide regular updates on the asset's performance, material changes, and upcoming events affecting repayment or distributions. This is not unique to tokenization. It is a standard obligation of any securities issuer, but it requires deliberate planning.

- What tokenization does not solve: It does not create liquidity where no investor demand exists. A vessel with weak charter prospects, uncertain repayment sources, or a borrower with limited operating history will not become a better investment because its financing instrument lives on a blockchain. Due diligence requirements do not diminish. Investor expectations around transparency and reporting do not diminish. Tokenization should be seen as an infrastructure improvement, not a credit enhancement.

—

InvestaX is a Singapore-based tokenization platform licensed by the Monetary Authority of Singapore, holding both a Capital Markets Services licence and a Recognised Market Operator licence. InvestaX supports the full lifecycle of tokenized real-world assets, from issuance and distribution to secondary market trading and custody for financial institutions, fund managers, and asset owners globally.

What types of maritime assets can be tokenized?

Commercial vessels of most types can serve as the underlying asset for a tokenized financing, including cargo ships, tankers, LNG carriers, tugs and barges, and container vessels. The asset needs to have a verifiable value, a clear legal ownership structure, and for debt instruments, a credible repayment source such as a charter contract or confirmed bank refinancing in progress.

What regulatory licence does a platform need to issue tokenized ship financing in Singapore?

In most cases, where tokenized maritime instruments are classified as securities in Singapore, a platform needs a Capital Markets Services (CMS) licence to manage issuance and distribution under Monetary Authority of Singapore regulations. If secondary trading is offered, a Recognised Market Operator (RMO) licence is also required.

This applies to the typical full-lifecycle model. Requirements may vary depending on the deal structure, distribution scope, and whether secondary trading is included.

How are distributions handled for tokenized maritime assets?

Distributions - whether interest payments on a bridge loan or charter revenue shares on an equity instrument - are paid on a defined schedule. Smart contracts can automate allocation to token holders. Payments may be made in fiat, stablecoins, or both.

What is the minimum deal size for a tokenized vessel financing?

There is no fixed regulatory minimum, but practical economics generally favour deals of $1 million or more. The legal structuring, compliance, and platform costs associated with a tokenized securities offering are relatively fixed regardless of deal size. Below a certain threshold, these costs consume a disproportionate share of the financing raised.

InvestaX's RWA tokenization platform, which operate on a SaaS-based model, allow issuers to run repeatable programmes and issue multiple RWA tokens over time using the same legal and infrastructure setup. This improves cost efficiency and makes smaller deals more viable on a programmatic basis.