The vault sector is attracting institutional capital at scale. Kraken launched DeFi Earn in January 2026, routing exchange deposits into on-chain vaults and crossing $150M in AUM. Morpho's vault ecosystem now holds over $10 billion in stablecoin TVL, and Bitwise - a global crypto asset manager with $11 billion in client assets - launched an allocation vault on Morpho in January 2026.

Inside this broader movement, a distinct category is gaining ground: the real world asset vault, or RWA vault, where the yield comes from real-world financial assets (RWA) managed by financial institutions such as Franklin Templeton, BlackRock, and Fidelity.

Understanding what makes this category different, and why stablecoin capital is increasingly flowing into it, is relevant for any platform that holds stablecoin balances today.

Key takeaways

- RWA tokenization puts real-world assets on-chain. A real world asset vault takes that a step further. It is the on-chain structure that lets stablecoin capital flow directly into those assets without leaving the on-chain environment and without building asset management or compliance infrastructure in-house.

- Platforms with stablecoin balances can route that capital into an RWA vault and access regulated, asset-backed yield without leaving the on-chain environment or requiring conversion to fiat.

- InvestaX is a MAS-licensed tokenization platform in Singapore offering regulated RWA vault infrastructure for platforms holding stablecoin balances. Contact InvestaX to discuss a partnership.

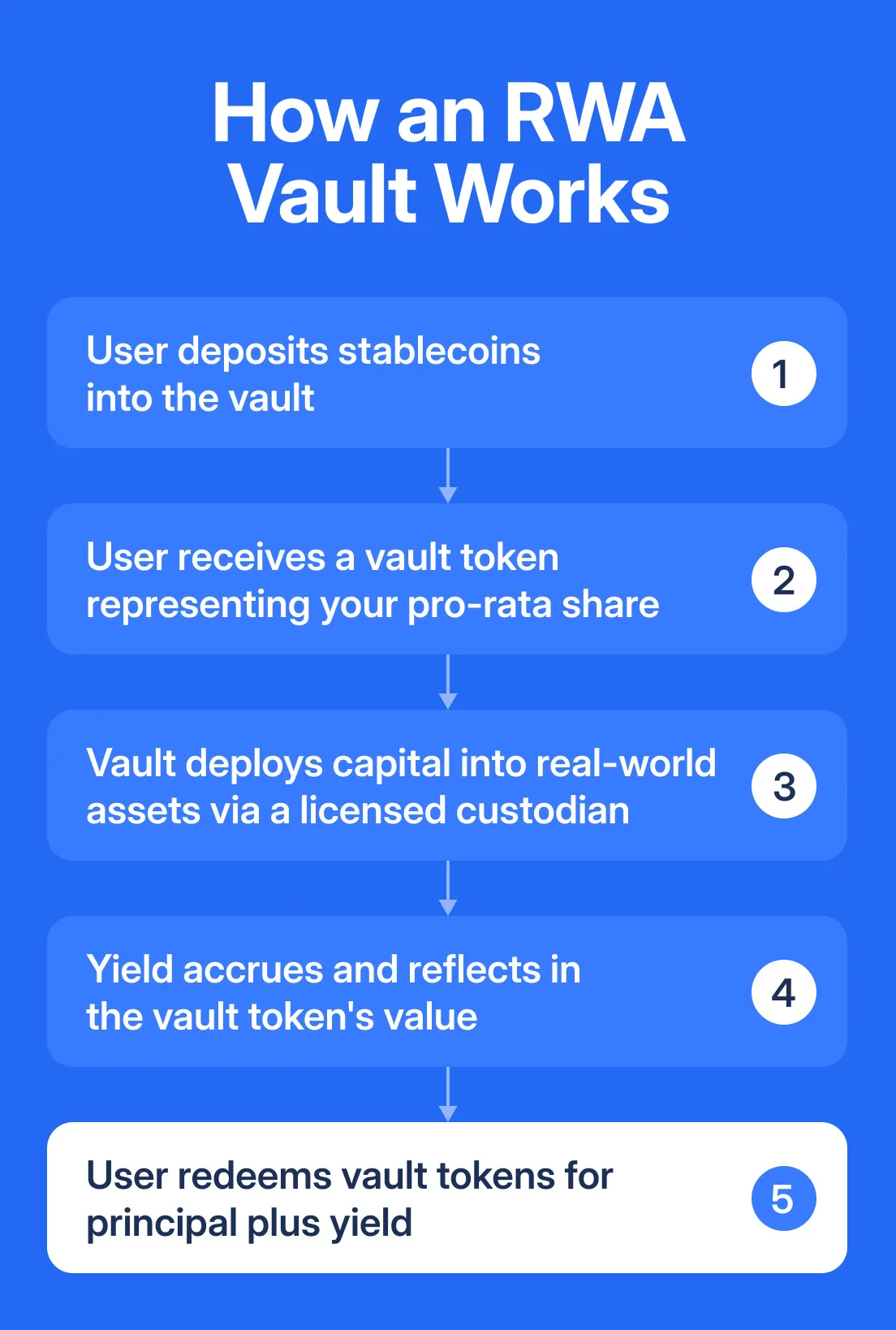

What is an RWA vault, and how does it work

A real world asset vault (RWA vault) is an on-chain fund structure that holds a tokenised claim on a real-world asset and issues a token representing a depositor's pro-rata share.

Two things define the category.

- The first is regulation. An RWA vault is a regulated product with an on-chain interface. The custodian holding the underlying asset is licensed, and deposit, redemption, and settlement activity sits inside a defined regulatory framework.

- The second is the yield source. The underlying assets are real-world financial instruments: money market funds, government bonds, corporate bonds, private credit. Yield flows from economic activity, such as bond coupon payments, T-bill interest, and loan repayments from private credit borrowers.

In practice, the flow may work as follows.

As Julian Kwan, CEO of InvestaX, described it: the vault is the wrapper, the standard, and the rail. The underlying asset sits with a licensed custodian. The vault token is the on-chain claim.

Why stablecoin capital flows naturally into RWA vaults

RWA vaults are on-chain. Stablecoins are on-chain. Two instruments that exist in the same environment are structurally easier to connect, stablecoin capital can route into a vault without leaving the on-chain world, without requiring conversion to fiat, and without the settlement friction that typically exists when capital moves between different rails. That structural compatibility is part of why stablecoin capital and RWA vaults are increasingly discussed together.

Stablecoin transaction volume reached approximately $33 trillion in 2025, with Visa's stablecoin settlement hitting a $4.5 billion annualised run rate by January 2026. In EY-Parthenon's 2025 stablecoin survey, 13% of corporates and financial institutions reported using stablecoins, and 54% of non-users expected to adopt within six to twelve months. As stablecoin capital grows and institutionalises, the question of what to do with idle balances between transactions becomes increasingly material. For a platform holding $100 million in stablecoin float between settlement cycles, leaving that capital undeployed is a meaningful operational cost. (YellowSage Journals)

The RWA vault provides a route to put that capital to work in regulated, real-world assets while it remains on-chain. The depositor sends stablecoins in and receives a vault token as their claim. The underlying assets generate yield through real economic activity. The structure does not require leaving the on-chain environment or building the asset management, custody, or compliance infrastructure in-house.

DeFi vault yield and RWA vault yield: what the data shows

If you have been in the crypto industry for a while, you are likely familiar with DeFi vaults. Platforms like Morpho, Aave, and Yearn allow depositors to earn yield by lending stablecoins to crypto borrowers, providing liquidity, or running automated yield strategies. This model works and has generated meaningful returns for participants, particularly during periods of strong crypto borrowing demand.

The structural dynamic changes when market conditions shift. DeFi lending rates are correlated with crypto borrowing demand -- when sentiment falls, borrowing activity and associated yields tend to fall with it. Aave's USDC yield sat at approximately 2.61% in April 2026, below the 3.14% offered by conventional cash management accounts in the same period. That does not mean DeFi yield is structurally inferior -- it means it behaves differently from yield linked to real-world financial activity, and that difference matters for how a platform thinks about offering yield to its users. (White House)

RWA vault yield comes from bond coupon payments, T-bill interest, and private credit loan repayments. These returns are generated by real economic activity and are generally less correlated to crypto market conditions. One of the most important shifts in this cycle is that yield is no longer the primary differentiator. Risk management is. That observation applies directly to the RWA vault category. The question a platform should ask is not just what yield a vault advertises, but where that yield comes from, who manages the underlying assets, and what happens during a redemption. (Perkins Coie)

In the RWA vault model, those questions have specific answers. The underlying assets are managed by institutional names with audited funds: BlackRock iShares ETFs, Fidelity money market funds, Franklin Templeton's OnChain US Dollar Money Market Fund, Matrixdock's STBT backed by short-term US Treasuries. The vault token is a claim on those assets. That accountability chain is different from what exists in a DeFi pool.

DeFi yield and RWA vault yield serve different purposes and different user profiles. The more relevant question for most platforms is not which is better, but which fits their regulatory environment, their users, and their risk tolerance.

What sits inside an RWA vault, and why the asset matters

RWA vaults hold tokenised claims on real-world financial assets managed by regulated institutions. As of 2026, the most common asset types found in vaults include:

- Money market funds and short-term government bonds. Backed by sovereign debt or high-quality short-duration credit, with daily or near-daily liquidity. For example, InvestaX offers tokenised exposure to the Franklin Templeton OnChain US Dollar Money Market Fund and Matrixdock's STBT, which holds short-term US Treasuries.

- High-yield corporate bonds. Publicly traded bonds offering higher yield than government instruments in exchange for greater credit risk. The underlying bonds trade on public markets, providing price transparency and liquidity. For example, InvestaX's HYCB vault holds exposure to BlackRock's iShares high-yield corporate bond ETF, a structure well-suited to institutional carry strategies.

- Private credit. Loans to businesses or trade finance positions, typically offering higher yield in exchange for longer lock-up periods and less secondary liquidity. The higher yield reflects the illiquidity premium and the credit risk of the underlying borrowers.

When platforms holding stablecoin balances evaluate an RWA vault partnership, the key questions are where the yield comes from, who custodies the underlying assets, and how redemption works in practice. Clarity on those three points gives any platform a reliable basis for evaluating whether a vault structure fits their risk profile and regulatory environment.

Who this is relevant for

Any platform that holds stablecoin balances, whether in its own treasury or on behalf of users, sits in a structurally similar position: capital that could be earning is sitting idle between transactions. The specific business model varies. Crypto exchanges hold user USDC between trades. Payment platforms carry settlement float. Neobanks and fintechs route user balances through stablecoin rails. Wallet providers hold stablecoins on behalf of users who park them between transactions. In each case, the idle capital represents a yield opportunity that currently goes unaddressed.

For these platforms, the RWA vault addresses that gap in two ways:

- Deploying their own treasury float into a licensed vault and earning directly on idle capital

- Offering users a regulated yield product without building the licensing, asset management relationships, or compliance infrastructure themselves.

Both paths are already available via InvestaX. Which one fits depends on the platform's regulatory environment and how it wants to position the product to users.

Why this matters now

Two structural forces are converging to make this moment commercially relevant.

The GENIUS Act, signed into law in July 2025, prohibits payment stablecoins from paying yield directly to holders, pushing yield generation into a separate yield-generation layer including RWA tokens. Platforms holding stablecoin balances on behalf of users are positioned to offer that yield through an RWA vault without being the stablecoin issuer.

At the same time, institutional stablecoin adoption is scaling rapidly. Visa's stablecoin settlement hit a $4.5 billion annualised run rate by January 2026, with market capitalization at $312 billion and projections pointing toward $1 trillion by late 2026. Mentions of "stablecoins" in public company filings increased 290% year-over-year in 2025. As institutional capital flows into stablecoin infrastructure at this scale, the demand for compliant, auditable yield grows with it, and that demand is increasingly directed toward regulated RWA vault infrastructure.

The vault infrastructure to address that demand is live and licensed. For platforms that have not yet added a regulated yield tier, the window to differentiate before this becomes standard across exchanges, wallets, and payment products remains open.

Getting started

InvestaX is a MAS-licensed tokenization platform in Singapore. We help fintech platforms and digital asset businesses access regulated, asset-backed returns on stablecoin balances, or offer it as a product to their users.

For a market overview of the yield-bearing stablecoin category, read The Rise of Yield-Bearing Stablecoins. For a practical guide on how platforms integrate and what the revenue model looks like, read Stablecoin Yield Backed by Real Assets: A Guide for Fintech Platforms. To start a conversation about what a partnership could look like for your platform, contact InvestaX.

What is an RWA vault?

An onchain real world asset vault (RWA vault) is essentially an onchain fund structure. On the technical side, an RWA vault is an onchain structure that holds a tokenised claim on a real-world asset and issues a token representing a depositor's pro-rata share. The underlying assets - which may include money market funds, government bonds, corporate bonds, or private credit - are held by licensed custodians and managed by regulated asset managers. Yield flows from real economic activity such as bond coupon payments or loan repayments, and accrues to vault token holders.

How is an RWA vault different from a DeFi vault?

A DeFi vault generates yield from crypto-native activity such as lending to crypto borrowers, providing liquidity, or running automated trading strategies. An RWA vault generates yield from real-world financial instruments managed by regulated institutions. The yield sources are different, the risk profiles are different, and the regulatory structures are different. Both models exist and serve different purposes.

Can stablecoins be deposited directly into an RWA vault?

RWA vaults are on-chain smart contracts, and stablecoins are on-chain instruments, which makes them structurally compatible. In many RWA vault structures, depositors can send stablecoins such as USDC or USDT directly into the vault and receive a vault token representing their share. InvestaX's RWA vaults are structured this way, accepting stablecoin deposits and issuing vault tokens that represent a depositor's pro-rata claim on the underlying assets.

What does InvestaX offer in this space?

InvestaX is a MAS-licensed tokenization platform in Singapore providing regulated vault infrastructure for fintech platforms, digital asset businesses, and platforms holding stablecoin balances. Platforms can access regulated, asset-backed returns on their stablecoin treasury or offer a yield product to their users via API integration.